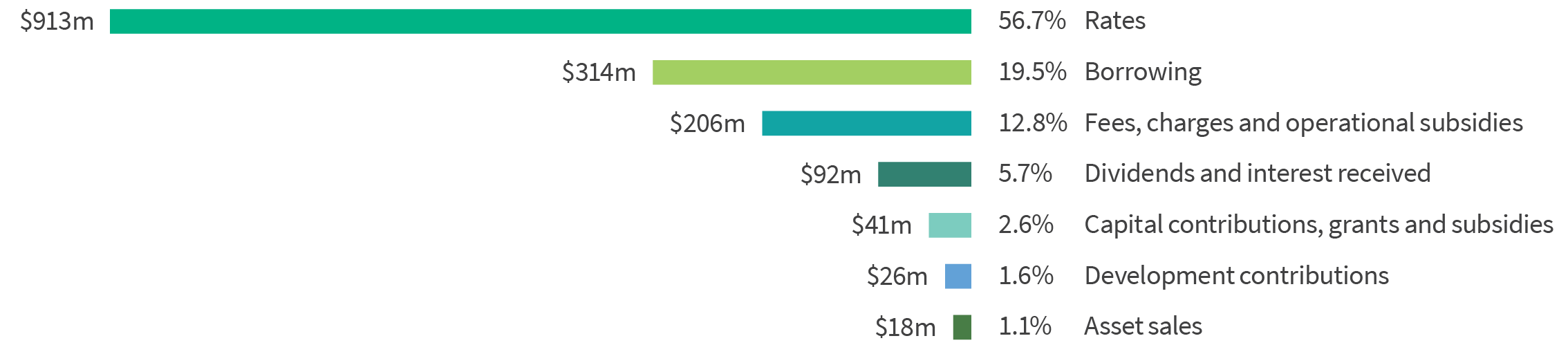

Rates provide 57% of the Council’s funding for the services and activities that keep Christchurch functioning.

In the Long Term Plan, we proposed an average rates increase of 5.80% for 2026/27. We are now proposing an overall average rates increase of 7.96%. Of this, 1.02% is going towards One New Zealand Stadium at Te Kaha.

The proposed rates increase is higher than planned in the LTP – 2.06% of the proposed increase is due to our use of an operating cash surplus from 2024/25 to keep rates affordable in 2025/26. This was a one-off reduction for that year. The proposed three-year cumulative rates increase in 2026/27 is 26.47%, compared to the cumulative increase in the LTP of 26.13%.

Under this proposal, the Council would collect $912.6 million (excluding GST) in rates to help fund essential services, capital renewal and replacement projects, and community events and festivals. This revenue is supplemented by funding from fees and charges, government subsidies, interest, dividends from subsidiaries and development contributions. Borrowing is used to fund a significant portion of the capital programme.

Where our funding of $1611m will come from in 2026/27

Proposed changes to rates

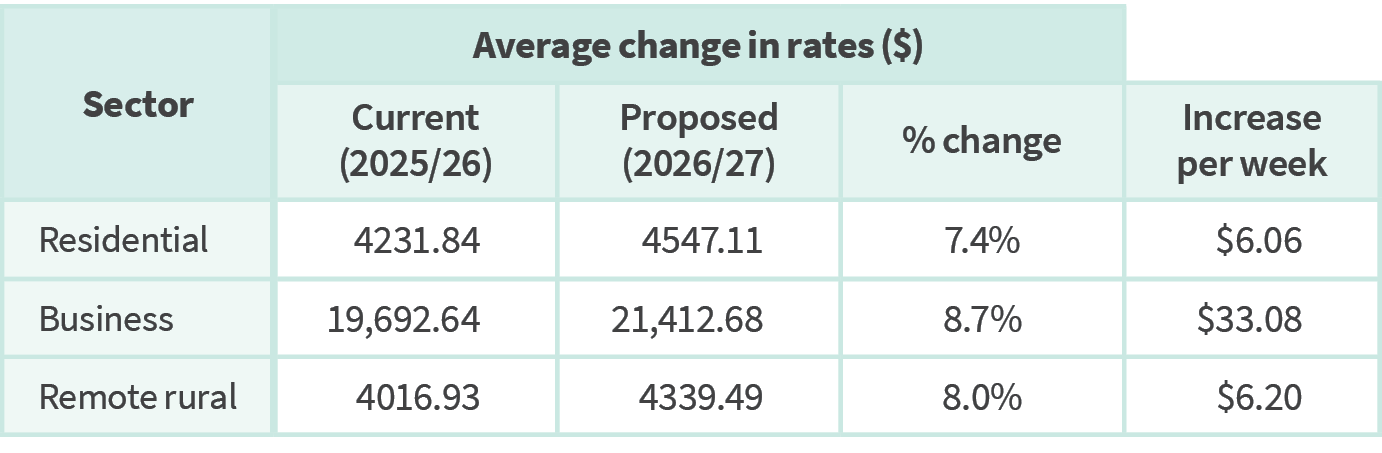

For the typical household, our proposed average rates increase for 2026/27 is 7.4%.

The average proposed rates increase across all ratepayers – households, and business and rural properties – is 7.96%.

Rates for an individual property will depend on:

- The property’s classification (whether it’s a standard, business or remote rural property).

- Which rates the property pays (for example, a property only pays the sewer rate if it’s within the sewer serviced area).

- The capital value of the property.

- How many ‘separately used or inhabited parts’ (SUIPs) the property has. Fixed rates are paid based on the number of SUIPs. For example, a property with two flats will pay two fixed charges. Most residential properties have only one SUIP.

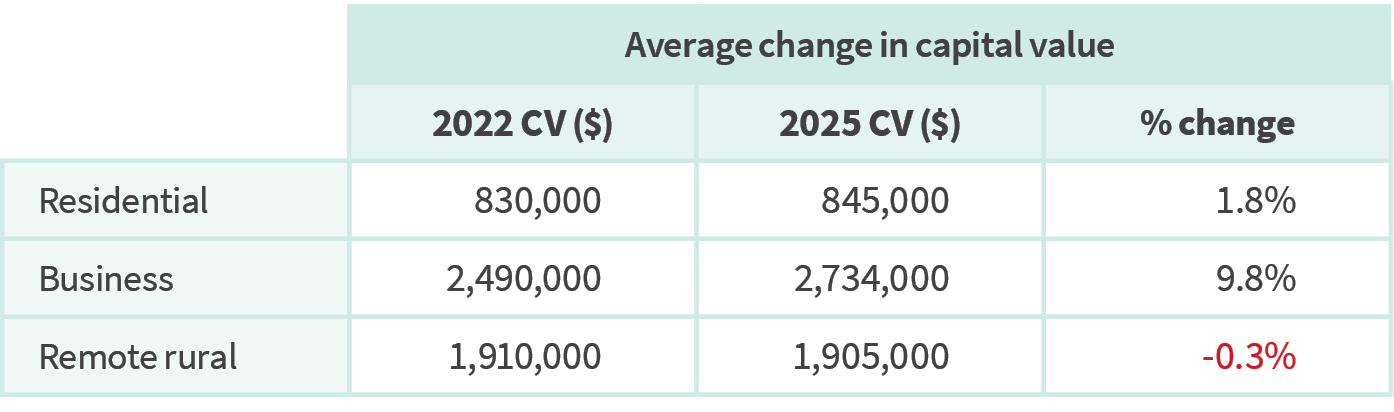

The 2025 revaluation

Every three years, the Council is legally required to carry out a citywide revaluation of every property for rating purposes.

Quotable Value NZ has recently completed its latest revaluation, based on market values as at 1 August 2025, and the new valuations will apply from 1 July 2026. This revaluation shows a relatively small average increase across the whole district of 3.4%, but with some significant differences between types of property as shown below.

The revaluation doesn’t affect the total rates collected by the Council, but it does affect how this is shared out between property owners. To help even out the distribution of rates, we’re proposing a change to what we call a differential – see the bottom of the page for more.

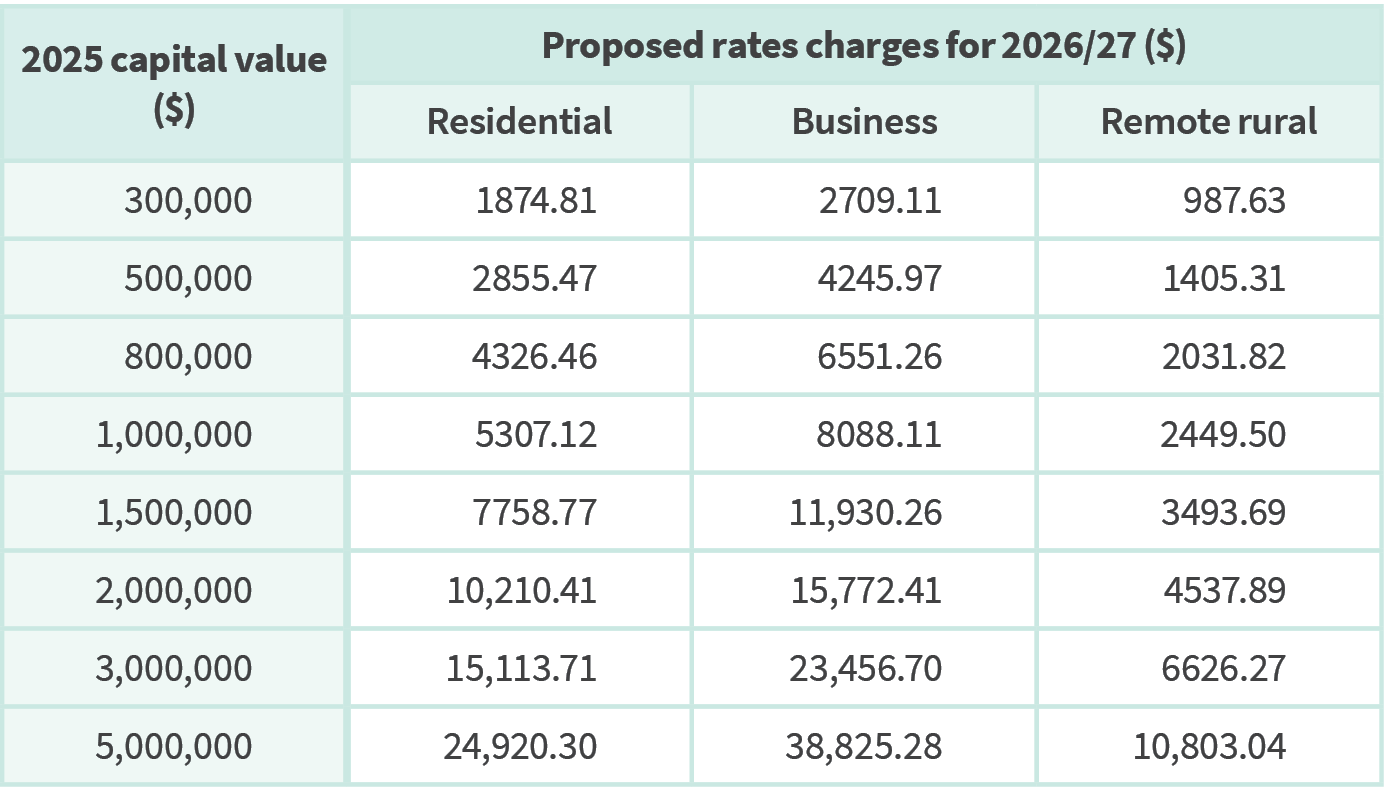

The table below shows examples of proposed rates for each of the three sectors next year based on the 2025 valuation. All rates figures include GST but do not include rates charged by Environment Canterbury.

Actual rates changes from 2025/26 will vary for each property – properties with valuation increases that have increased by more than average will get a higher rates increase, and those that have increased by less than average, or decreased, will get a lower rates increase.

The table below shows the rates for the average value property in each sector, and the resulting proposed weekly increase in rates.

These increases relate to Christchurch City Council’s rates, not to Environment Canterbury’s rates. As we collect these on Environment Canterbury’s behalf, you’ll also see their rates on your invoices.

Environment Canterbury is also asking for feedback on its Annual Plan 2026/27 at ecan.govt.nz/annualplan26. Feedback closes on 11.59pm on 31 March.

Our proposed change to the business differential on the general rate

This year’s significant increase in business property valuations will move more of the rates burden from residential to business ratepayers. Without some action from the Council, this will increase rates for most business ratepayers materially more than it will for most residential ratepayers.

At present, business properties account for 19% of the city’s capital value and pay 26% of all our total rates. To keep the proportion of rates paid by business properties the same, we’re proposing to decrease the general rate business differential from 2.22 to 2.00.

This means a business property currently pays general rates at 2.22 times what a standard (residential) property with the same capital value pays. For a $1 million property, the difference is currently $3122.64 (including GST). Our proposed differential of 2.00 would keep the overall proportion of rates paid by the business sector about the same. This reflects the concept that the relative benefits they get from the Council’s services haven’t changed significantly, and means the rates increases for business ratepayers are more affordable, with increases in both sectors closer to the overall average.

The differential doesn’t apply to targeted rates like sewerage or water supply. We’ll keep the remote rural differential unchanged at 0.75.

We want to hear what you think

Do you have any feedback on our proposal to lower the differential paid by business property owners from 2.22 to 2.00 to keep the current overall proportion of rates paid by business and residential ratepayers the same? Do you have any alternative proposals?

Our proposed change to the definition of short-term accommodation

For the purposes of rating, we treat residential properties used for un-hosted short-term accommodation as businesses, and charge them the business rate differential.

Our current policy only applies to properties that are rented out for more than 60 days per year, have a resource consent for the purpose of short-term accommodation, or are used mainly for hosted short-term accommodation.

Because it’s difficult to determine the amount of time a property is used for short-term accommodation, the current policy is hard to apply, and we’re not charging short-term accommodation providers the business rate differential. This means these ratepayers aren’t paying their fair share, and leaves other ratepayers to pick up the slack.

We’re proposing to simplify the definition of short-term accommodation by removing the 60-day requirement from our rating policy. This would mean that if the primary use of the rating unit is short-term accommodation (hosted or un-hosted), or if it has a resource consent for that use, we will consider it as short-term accommodation and treat it as a business for rating purposes.

It’s important to keep in mind that the Council sets rates based on its revenue requirements. If we can identify a property as a short-term accommodation provider, we won’t collect any additional revenue – it will simply change the distribution of who pays the rates.We want to hear what you think

Do you have any feedback on our proposal to remove the 60-day requirement from the definition of short-term accommodation for the purposes of the rating policy? Do you have any alternative proposals for how the Council could identify short-term accommodation providers?

Excluding property-based rates, which are our biggest source of revenue, our total revenue for 2026/27 is $360.6 million – $37.2 million lower than projected in the LTP. The big changes are:

- Reduced funding for the capital programme, due to an overstatement in the LTP ($33.6 million).

- Reduced interest revenues, due to lower interest rates, and lower on-lending to subsidiaries ($13.7 million). This will be offset by lower interest costs.

- Reduced Hagley Park parking fees, due to lower usage than anticipated in the LTP ($1.4 million).

- Additional revenue of $7.2 million from Burwood Landfill.

- An additional $6.2 million of subvention receipts planned.

We propose $314.4 million of new borrowing in the Draft Annual Plan to help us deliver our capital programme in 2026/27 – $37.9 million lower than planned for in the LTP. We also propose to pay off $91.1 million of our existing debt.

Gross debt at 30 June 2027 is expected to be $2.89 billion, which is $565.9 million lower than planned in the LTP. This is primarily due to updating the capital programme expenditure for deliverability in the 2025/26 Annual Plan and the proposed 2026/27 Annual Plan. On top of that, the Council is borrowing less on behalf of its subsidiaries than planned in the Long Term Plan. Overall, 22.5% of Council rates will be allocated to debt servicing and repayment costs, which is slightly lower than the 24.2% originally projected in the LTP.

The Council’s borrowings are well within prudential limits. Borrowing enables us to spread the funding of infrastructure across multiple years, and for future ratepayers who will benefit to also contribute to the cost.We’re proposing to change some Council fees and charges in the Draft Annual Plan. We’re conscious of the financial pressure many of our residents and ratepayers are under, and we have attempted to avoid cost increases to the community that would create a barrier for them using our services. In other areas the proposed fee increase is in keeping with the increased costs the Council is facing. Fees in some areas are staying the same.

You can find more information about these proposed changes to our fees and charges from page 104 of the Draft Annual Plan.